In March 2026, Nigeria’s Debt Management Office offered a two-year government savings bond at 12.9% per annum. The three-year paid 13.9%. Minimum buy-in was ₦5,000. That’s about twelve US dollars.

Around the same time, Kenya’s Central Bank was auctioning 10-year government bonds at over 11%, with shorter-term Treasury bills paying around 8%, all tax-exempt for individual investors. These are sovereign instruments from two of Africa’s largest economies, open to retail buyers, paying rates that most developed-market debt hasn’t matched in over a decade.

And these are just two examples. Across emerging markets, from Colombia to Vietnam to Egypt, there are government bonds, trade finance facilities, invoice-backed credit lines, and working-capital structures offering real yield tied to real economic activity. Not speculative. Not synthetic. Real businesses needing real capital, willing to pay real rates for it.

So why is almost none of this accessible to the average person with a crypto wallet and capital to deploy?

• • •

The gap is not in the opportunity. It’s in the plumbing.

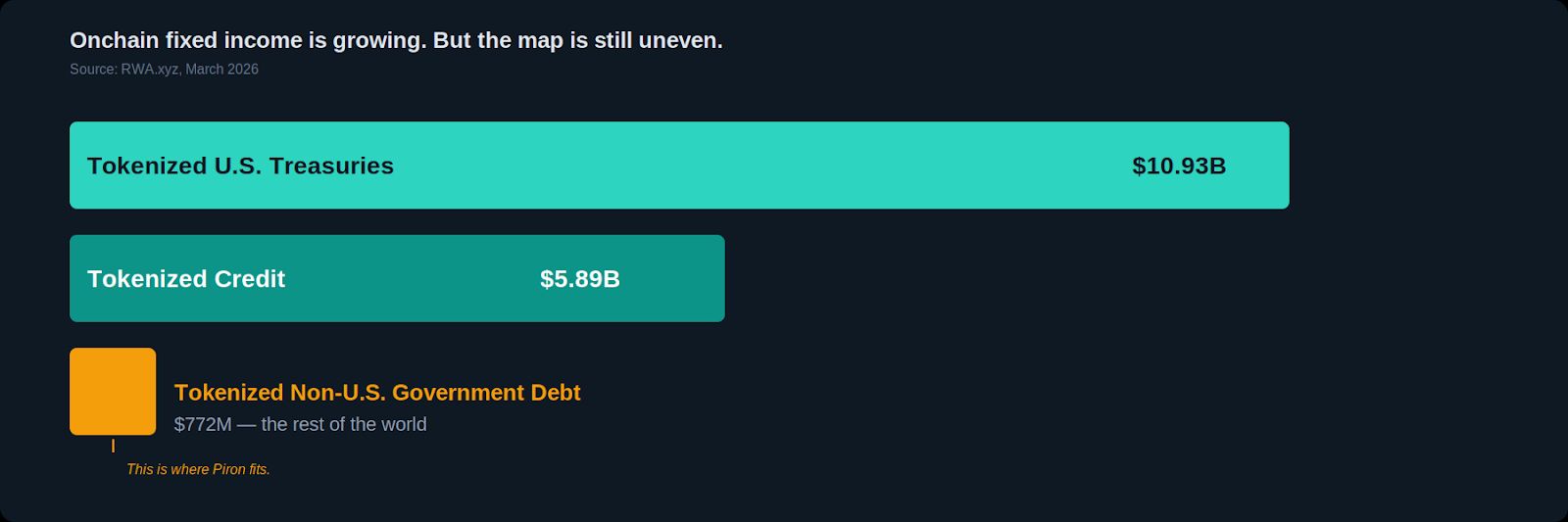

Look at where tokenized fixed income actually lives today. As of March 2026, tokenized U.S. Treasuries have crossed $10.93 billion on RWA.xyz. Tokenized credit sits at $5.89 billion across 881 assets. That’s meaningful progress and proof that serious financial instruments can exist onchain and attract serious capital.

But here’s the number nobody talks about: tokenized non-U.S. government debt, the entire rest of the world’s sovereign paper onchain, stands at $772 million. Total.

That’s not a rounding error. That’s a map with most of the world missing from it.

The reason isn’t that the opportunities don’t exist. It’s that the product layer around them doesn’t. Emerging-market fixed income still lives behind the same walls it always has: fragmented distribution, geographic restrictions, manual onboarding, opaque structures, and the kind of institutional gatekeeping that makes access a function of who you know rather than what you’re willing to learn.

If you’re a fund with the right prime broker relationships, you can navigate this. If you’re anyone else, a crypto-native allocator, a diaspora investor, someone in Lagos or Nairobi who actually lives in these economies, good luck figuring out what’s available, what backs it, what the duration is, what the fees are, or what happens if something goes wrong.

That is the gap Piron exists to close.

• • •

What we’re building

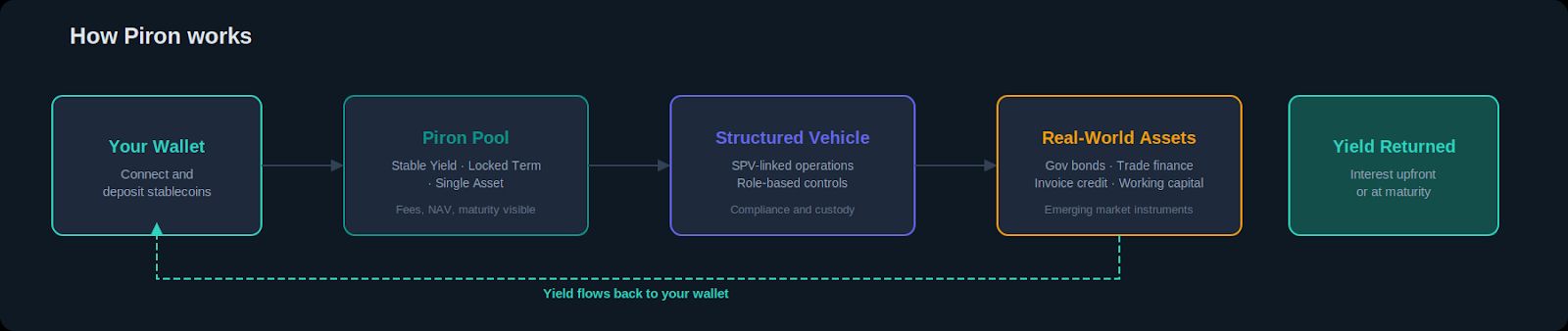

Piron is a wallet-native access layer for emerging-market fixed income.

We sit between global capital and local yield opportunities, and we build the product experience that makes those opportunities legible, comparable, and accessible through a wallet. Without stripping out the information you need to make real decisions.

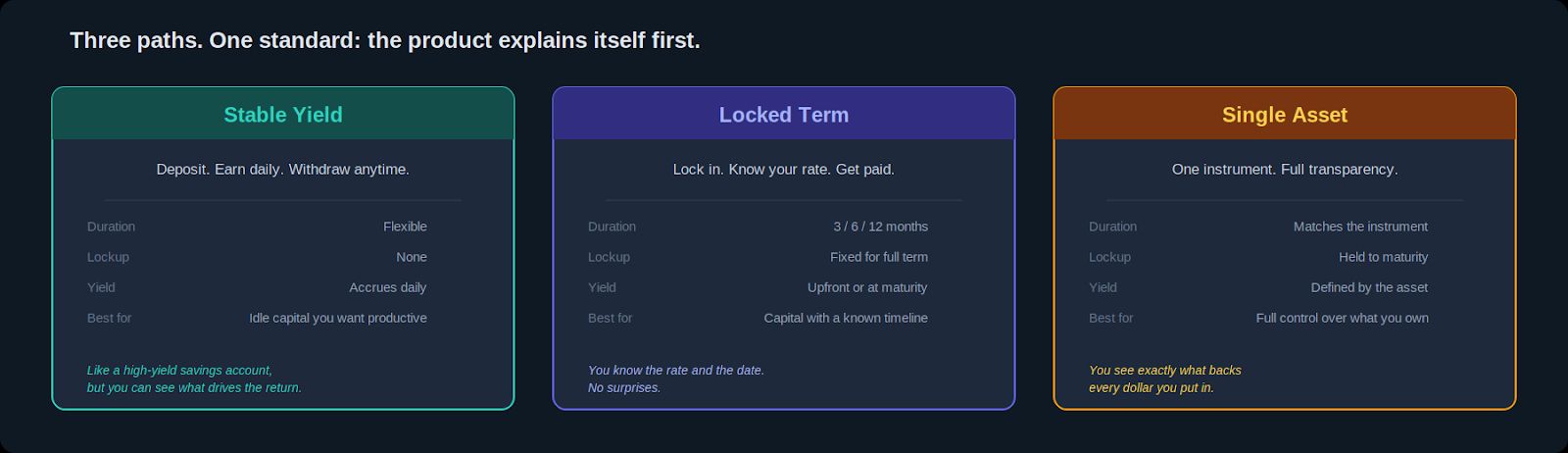

At launch, Piron organizes opportunities into three paths. Each one is designed around a different way people actually think about putting capital to work.

Stable Yield

Deposit into a pool. Earn yield daily. Withdraw when you need to. This is for capital you want working for you without tying it down. Think of it like a high-yield savings account, except you can see exactly what’s generating the return underneath.

Locked Term

Pick your duration: 3 months, 6 months, 1 year. Lock your capital. Receive your interest upfront or at maturity. You know the rate, you know the timeline, and you know what you’re getting before you commit. Simple as that.

Single Asset

One specific instrument. One maturity date. Full visibility into what backs it. No broad pool, no blended exposure. You pick the exact opportunity, you see exactly what you own, and you hold it to maturity. This is for people who want to know the full story behind every dollar they deploy.

Behind all three is a structured operating layer: pool lifecycles, NAV mechanics, fee transparency, SPV-linked operations, and role-based access controls. That’s the kind of infrastructure that doesn’t make for exciting marketing copy, but it’s the difference between a yield product that works and one that works until it doesn’t.

We’re not interested in hiding that complexity. We’re interested in building it well enough that the experience on top can feel simple without being misleading.

• • •

Why this matters beyond crypto

There’s a framing that treats emerging-market yield as a niche crypto play, an exotic corner of the RWA narrative. We think that gets it exactly backward.

The IFC estimates that formal small and medium enterprises across developing economies face a $5.7 trillion financing gap. That’s not a footnote in a research paper. That’s the distance between how much productive capital these economies need and how much actually reaches them through existing channels.

When a Nigerian manufacturer needs working capital to fulfill an export order, or a Kenyan agribusiness needs to finance a harvest cycle, or a Colombian logistics company needs to bridge receivables, those are real credit needs generating real yields. The capital willing to meet those needs exists. The infrastructure connecting the two is what’s broken.

Piron doesn’t fix all of that. But we believe that building a better product layer, one where yield opportunities are transparent, structured, and accessible through modern rails, is how the map starts filling in.

• • •

How we think about this

We have a few convictions that shape everything we’re doing.

The product should explain itself before it asks for your money

Duration, fees, liquidity conditions, asset exposure, downside scenarios. All of it should be visible before you commit. Not buried in docs. Not available "on request." Front and center.

Risk should stay visible

We’re not building Piron to make risk disappear. We’re building it to make risk easier to see. There’s a meaningful difference between a product that hides its risks and one that helps you understand them. We want to be the second.

Access should scale without losing clarity

Making emerging-market fixed income easier to reach is only valuable if people can actually evaluate what they’re reaching for. Otherwise you’re just moving the problem from "you can’t get in" to "you’re in but you don’t know what you bought."

We’d rather grow slowly and get the standard right than scale fast on vibes and a big APY number.

• • •

Why now

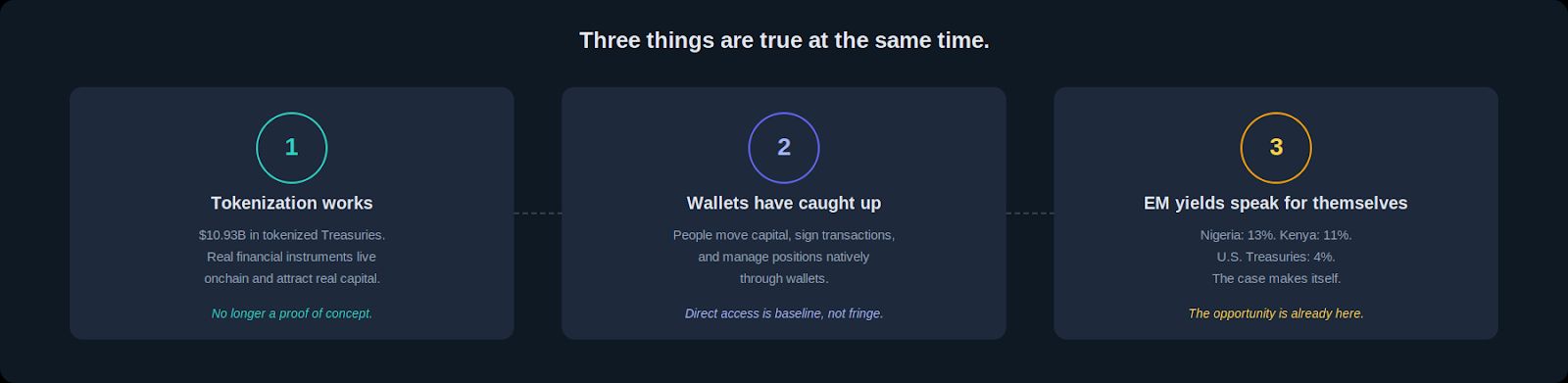

Three things are true at the same time, and that’s what makes this moment different.

Tokenization has graduated from proof-of-concept to production. Wallet UX has caught up to where direct, programmable access is baseline. And the yield environment in emerging markets makes the case on its own. When a Nigerian government bond pays 13% and a Kenyan 10-year bond pays 11% while a U.S. Treasury pays 4%, the conversation about where capital should be able to flow stops being theoretical.

What’s missing is the product layer that connects these three things. That’s Piron.

• • •

We’re starting in public

Piron’s testnet is live today.

We’re launching publicly because we believe the standard for how onchain yield products get built, especially in emerging markets, should be set early. Not retrofitted after the market scales past the point where anyone cares.

We’re early. The product will evolve. Things will break. But the thesis won’t change: if fixed income is going to become more open, more programmable, and more global, it also needs to become more understandable.

That’s what we’re here to build.

Explore Piron testnet at piron.finance